http://rt.com/usa/californians-outraged-police-armored-vehicle-689/

Monday, December 23, 2013

Tuesday, December 17, 2013

Monday, December 9, 2013

Wednesday, November 27, 2013

New German Coalition (A Prophetic Piece?)

New German Coalition Pledges Billions in New Spending - Wall Street Journal

http://tinyurl.com/q44cqln

shared via www.newshog.co

US B-52 Flies Over China Air Zone

http://www.cnn.com/2013/11/26/world/asia/china-us-b52s/index.html?c=homepage-t

Tuesday, November 26, 2013

Saturday, November 23, 2013

Thursday, November 21, 2013

U.S. Debt Culture and the Dollar's Fate | The National Interest

U.S. Debt Culture and the Dollar's Fate | The National Interest

We are well-past the threshold of 70% debt to our National GDP. No economy has survived that pushed past this critical point. At some point, our debt-system must give way to a new method and means of commerce and exchange in order to be viable and solvent in the face of growing economies and currencies such as the Chinese Yuan, the trading bloc of Europe, BRICS, Opec, etc.- FS

We are well-past the threshold of 70% debt to our National GDP. No economy has survived that pushed past this critical point. At some point, our debt-system must give way to a new method and means of commerce and exchange in order to be viable and solvent in the face of growing economies and currencies such as the Chinese Yuan, the trading bloc of Europe, BRICS, Opec, etc.- FS

China's Planned Crude Oil Futures May Be Priced In Yuan - SHFE | Reuters

China's planned crude oil futures may be priced in yuan - SHFE | Reuters

Opec petro-dollars have historically been the U. S. Dollar - that is, until now. This represents what could be one of the most serious blows to the destabilizing of the U. S. Dollar and the end of its status as the global reserve currency.

Opec petro-dollars have historically been the U. S. Dollar - that is, until now. This represents what could be one of the most serious blows to the destabilizing of the U. S. Dollar and the end of its status as the global reserve currency.

Friday, November 8, 2013

United States Of Europe

http://www.telegraph.co.uk/news/worldnews/europe/eu/10436218/David-Cameron-must-embrace-Churchills-vision-of-United-States-of-Europe.html

Monday, November 4, 2013

IMF Assesses Global Economics

IMF changes tune on global economic assessment - Financial Times

http://tinyurl.com/kdcs4my

shared via www.newshog.co

Thursday, October 31, 2013

Bitcoin App Choice Of Anti-Christ

http://www.forbes.com/sites/andygreenberg/2013/10/31/darkwallet-aims-to-be-the-anarchists-bitcoin-app-of-choice/

Wednesday, October 30, 2013

U.S. Debt Problems 'Casting Global Shadow': EU's Barroso - Yahoo News

U.S. debt problems 'casting global shadow': EU's Barroso - Yahoo News

It is not unreasonable to imagine that at some point the global community will become intolerant of our lack of fiscal and political responsibility and ban together to force us into a compliance that lessens our threat to the global economy does so at a high cost to our sovereignty. - FS

It is not unreasonable to imagine that at some point the global community will become intolerant of our lack of fiscal and political responsibility and ban together to force us into a compliance that lessens our threat to the global economy does so at a high cost to our sovereignty. - FS

Sunday, October 27, 2013

Friday, October 25, 2013

Breaking The Anti-Christ Spirit Over America

http://www.charismanews.com/index.php/?format=feed&type=rss

The 'Anti-Christ Spirit' is, in the simplest terms, that spirit of mankind seeking to cast off all restraint, especially that of the precepts of divine Scripture and the dynamics of the Kingdom of God. It is prevalent not only in the secular world but also in the lives of many (if not most) Christians in America who live with a predominant independence from God rather than a dependency upon God. - Freddie Steel

The 'Anti-Christ Spirit' is, in the simplest terms, that spirit of mankind seeking to cast off all restraint, especially that of the precepts of divine Scripture and the dynamics of the Kingdom of God. It is prevalent not only in the secular world but also in the lives of many (if not most) Christians in America who live with a predominant independence from God rather than a dependency upon God. - Freddie Steel

Is US Digging The Dollar's Grave?

http://www.marketoracle.co.uk/Article42760.html

I believe the dollar will not be able to compete with nor compete against the growing, global influence of trading blocs such as BRICS or the nations aligned with the Shanghai Cooperation Organization. These represent the largest trading bloc in the world and also are being courted by the Chinese Yuan for reserve currency status.

The concept of global commerce through closely aligned nations (such as the European Union, BRICS, etc.) causes the U. S. to be the Lone Ranger who much consider doing the same by aligning with Canada and Mexico in similar trading zones.

Should that be the case, we will eventually have ten, global trading zones/blocs. Some feel this could be what is referred to in apocalyptic literature as the ten nation Revived Roman Empire. However, I do not see that as being prophetically accurate. - Freddie Steel

I believe the dollar will not be able to compete with nor compete against the growing, global influence of trading blocs such as BRICS or the nations aligned with the Shanghai Cooperation Organization. These represent the largest trading bloc in the world and also are being courted by the Chinese Yuan for reserve currency status.

The concept of global commerce through closely aligned nations (such as the European Union, BRICS, etc.) causes the U. S. to be the Lone Ranger who much consider doing the same by aligning with Canada and Mexico in similar trading zones.

Should that be the case, we will eventually have ten, global trading zones/blocs. Some feel this could be what is referred to in apocalyptic literature as the ten nation Revived Roman Empire. However, I do not see that as being prophetically accurate. - Freddie Steel

World's First Bitcoin ATM Set to Go Live Tuesday | Wired Enterprise | Wired.com

World's First Bitcoin ATM Set to Go Live Tuesday | Wired Enterprise | Wired.com

Bitcoins are cryptocurrency for conducting global trade through peer-to-peer merchants. - Freddie Steel

Bitcoin (sign:

Bitcoin (sign:  ; code: BTC or XBT[8]) is a distributed peer-to-peer digital currency that functions without the intermediation of any central authority.[9] The concept was introduced in a 2008 paper by a pseudonymous developer known only as "Satoshi Nakamoto".[1]

; code: BTC or XBT[8]) is a distributed peer-to-peer digital currency that functions without the intermediation of any central authority.[9] The concept was introduced in a 2008 paper by a pseudonymous developer known only as "Satoshi Nakamoto".[1]

Bitcoin is called a cryptocurrency since it is decentralized and uses cryptography to prevent double-spending, a significant challenge inherent to digital currencies.[9] Once validated, every individual transaction is permanently recorded in a public ledger known as the blockchain.[9] The calculations required to authenticate Bitcoin transactions are completed using a network of private computers often specially tailored to this task.[10] As of May 2013, the Bitcoin network processing power "exceeds the combined processing strength of the top 500 most powerful supercomputers".[11] The operators of these computers, known as "miners", are rewarded with transaction fees and newly minted bitcoins. However, new bitcoins are created at an ever-decreasing rate.[9] Once 21 million bitcoins are distributed, issuance will cease.[9] As of August 2013, approximately 11.5 million bitcoins were in circulation.[12]

In 2012, The Economist reasoned that Bitcoin has been popular due to "its role in dodgy online markets,"[13] and in 2013 the FBI shut down one such service, Silk Road, which allowed the sale of illegal drugs for bitcoins. However, bitcoins are increasingly used as payment for legitimate products and services.[14] Notable vendors include Wordpress, OkCupid, Reddit, and Chinese Internet giant Baidu.[15]

Speculators have been attracted to Bitcoin, fueling volatility and price swings. In July 2013, Cameron and Tyler Winklevoss asserted that "there is relatively small use of bitcoins in the retail and commercial marketplace in comparison to relatively large use by speculators."[16]

The Bitcoin network protocol operates to provide solutions to the problems associated with creating a decentralized currency and a peer-to-peer payment network. Key among them is the use of a blockchain to achieve consensus and to solve the double-spending problem.

A bitcoin is defined by a chain of digitally-signed transactions that began with its creation as a block reward through bitcoin mining. Each owner transfers bitcoins to the next by digitally signing them over to the next owner in a Bitcoin transaction. A payee can then verify each previous transaction to verify the chain of ownership.

Bitcoin exchanges regularly fail, and the vast majority of transactions are completed on a single exchange that was originally a site for trading Magic: The Gathering cards online, Mt. Gox.

According to Reuters, undisclosed documents indicate that banks such as Morgan Stanley and Goldman Sachs have visited Bitcoin exchanges as often as 30 times a day. Employees of international banks and major financial organizations have shown interest in Bitcoin markets as well.[100]

Bitcoins have been described as lacking intrinsic value as an investment because their value depends only on the willingness of users to accept it.[106][107][108] In addition, a study indicated that 45 percent of Bitcoin exchanges end up closing with many customers losing their money.[109]

Like many assets, bitcoins are also subject to theft.

Derivatives on bitcoins are thinly available. One organization offers futures contracts on bitcoins against multiple currencies.[110]

Several bitcoin investors have become entrepreneurs in the evolving bitcoin universe. Efforts are underway to build financial services, new exchanges, and new payment products using bitcoin. Interest in the bitcoin sector has arisen from investment funds, with recent Peter Thiel's Founders Fund investing US$3 million in the sector and the Winklevoss twins making a US$1.5 million investment.[111]

Bitcoins are cryptocurrency for conducting global trade through peer-to-peer merchants. - Freddie Steel

Bitcoin

From Wikipedia, the free encyclopedia

| Bitcoin | |

|---|---|

A digital Bitcoin wallet

|

|

| Ledger | The majority of the Bitcoin peer-to-peer network regulates transactions and balances.[1][2] |

| Date of introduction | 3 January 2009 |

| Source | Bitcoin Genesis Block |

| User(s) | International |

| Issuance | Limited release |

| Source | Total BTC in Circulation |

| Method | The rate of new bitcoin creation will be halved every four years until there are 21 million BTC[3] |

| Subunit | |

| .001 | mBTC (millicoin) |

| .000001 | μBTC (microcoin) |

| .00000001 | satoshi[4] |

| Symbol | BTC, XBT,[5] |

A common Bitcoin logo.

Bitcoin is called a cryptocurrency since it is decentralized and uses cryptography to prevent double-spending, a significant challenge inherent to digital currencies.[9] Once validated, every individual transaction is permanently recorded in a public ledger known as the blockchain.[9] The calculations required to authenticate Bitcoin transactions are completed using a network of private computers often specially tailored to this task.[10] As of May 2013, the Bitcoin network processing power "exceeds the combined processing strength of the top 500 most powerful supercomputers".[11] The operators of these computers, known as "miners", are rewarded with transaction fees and newly minted bitcoins. However, new bitcoins are created at an ever-decreasing rate.[9] Once 21 million bitcoins are distributed, issuance will cease.[9] As of August 2013, approximately 11.5 million bitcoins were in circulation.[12]

In 2012, The Economist reasoned that Bitcoin has been popular due to "its role in dodgy online markets,"[13] and in 2013 the FBI shut down one such service, Silk Road, which allowed the sale of illegal drugs for bitcoins. However, bitcoins are increasingly used as payment for legitimate products and services.[14] Notable vendors include Wordpress, OkCupid, Reddit, and Chinese Internet giant Baidu.[15]

Speculators have been attracted to Bitcoin, fueling volatility and price swings. In July 2013, Cameron and Tyler Winklevoss asserted that "there is relatively small use of bitcoins in the retail and commercial marketplace in comparison to relatively large use by speculators."[16]

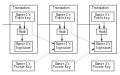

1.2 Payment network and mining

A diagram of a bitcoin transfer.

The Bitcoin network protocol operates to provide solutions to the problems associated with creating a decentralized currency and a peer-to-peer payment network. Key among them is the use of a blockchain to achieve consensus and to solve the double-spending problem.

A bitcoin is defined by a chain of digitally-signed transactions that began with its creation as a block reward through bitcoin mining. Each owner transfers bitcoins to the next by digitally signing them over to the next owner in a Bitcoin transaction. A payee can then verify each previous transaction to verify the chain of ownership.

3 Economics

Large fluctuations in the value of Bitcoin have led to criticism of its usefulness as a currency.[93] In addition, its deflationary bias encourages hoarding.[94] This reduces the the use value of a currency and has been the downfall of other private currencies.[95] However, currently Bitcoin does see some use as a currency[96] as well as being saved by individuals.[97]3.1 Exchanges

Through various exchanges, bitcoins are bought and sold at a variable price against the value of other currency. Bitcoin has appreciated rapidly in relation to other currencies including the US dollar, euro and British pound.[84][98][99]Bitcoin exchanges regularly fail, and the vast majority of transactions are completed on a single exchange that was originally a site for trading Magic: The Gathering cards online, Mt. Gox.

According to Reuters, undisclosed documents indicate that banks such as Morgan Stanley and Goldman Sachs have visited Bitcoin exchanges as often as 30 times a day. Employees of international banks and major financial organizations have shown interest in Bitcoin markets as well.[100]

3.2 Bitcoin as an investment

Although the Bitcoin Project describes bitcoin exclusively as an "experimental digital currency," [101] bitcoins are often traded as an investment.[102] Critics have accused bitcoin of being a form of investment fraud known as a Ponzi scheme.[103][104] A case study report[105] by the European Central Bank observes that the bitcoin currency system shares some characteristics with Ponzi schemes, but also has characteristics which are distinct from the common aspects of Ponzi schemes as defined by the U.S. Securities and Exchange Commission.Bitcoins have been described as lacking intrinsic value as an investment because their value depends only on the willingness of users to accept it.[106][107][108] In addition, a study indicated that 45 percent of Bitcoin exchanges end up closing with many customers losing their money.[109]

Like many assets, bitcoins are also subject to theft.

Derivatives on bitcoins are thinly available. One organization offers futures contracts on bitcoins against multiple currencies.[110]

Several bitcoin investors have become entrepreneurs in the evolving bitcoin universe. Efforts are underway to build financial services, new exchanges, and new payment products using bitcoin. Interest in the bitcoin sector has arisen from investment funds, with recent Peter Thiel's Founders Fund investing US$3 million in the sector and the Winklevoss twins making a US$1.5 million investment.[111]

Virtues Of Cryptocurrency

http://www.pbs.org/newshour/rundown/2013/10/a-bitcoin-evangelist-on-the-virtues-of-cryptocurrency.html

SEPA (Single Euro Payments Area), Precursor To The Mark Of The Beast?

http://m.us.wsj.com/articles/SB10001424052702304799404579155242624329108?mg=reno64-wsj

The Single Euro Payment System could be viewed as the precursor to the set up of an international, global business and trade system utilizing cashless transactions (cryptocurrency). As it is adopted in the European Union and becomes fine-tuned, it will become the standard imposed upon society as the only means to buy, sell, trade or borrow. It will eventually mutate into a total identification system that will include data necessary for travel and universal health care, etc. - Freddie Steel

The Single Euro Payments Area (SEPA) is a payment-integration initiative of the European Union for simplification of bank transfers denominated in euro. As of March 2012, SEPA consists of the 28 EU member states, the four members of the EFTA (Iceland, Liechtenstein, Norway and Switzerland) and Monaco.

The project includes the development of common financial instruments, standards, procedures, and infrastructure to enable economies of scale. This should, in turn, reduce the overall cost to the European economy of moving capital around the region (estimated as two to three percent of total GDP).[3]

The European Commission has established the legal foundation through the PSD. The commercial and technical frameworks for payment instruments were developed by the European Payments Council (EPC), made up of European banks. The EPC is committed to delivering three pan-European payment instruments:

Businesses, merchants, consumers and governments are also interested in the development of SEPA. The European Associations of Corporate Treasurers (EACT), TWIST, the European Central Bank, the European Commission, the European Payments Council, the European Automated Clearing House Association (EACHA), payments processors and pan-European banking associations – European Banking Federation (EBF), European Association of Co-operative Banks (EACB) and the European Savings Banks Group (ESBG) – are playing an active role in defining the services which SEPA will deliver.

Since January 2008, banks have been switching customers to the new payment instruments. By 2010, the majority were expected to be on the SEPA framework. As a result, banks throughout the SEPA area (not just the Eurozone) need to invest in technology with the capacity to support SEPA payment instruments.

SEPA clearance is based on the IBAN bank-account identification and the SWIFT-BIC bank identifier. Domestic transactions are routed by IBAN; earlier national-designation schemes will be abolished by February 2014, providing uniform access to the new payment instruments. By February 2016 consumers must drop BIC sorting information for SEPA transactions, since it will be derived from the IBAN for all banks in the SEPA area.

Multinational businesses and banks have the opportunity to consolidate their payment processing on common platforms across the Eurozone. They will benefit from the efficiency of choosing among competing suppliers, offering a range of solutions and operating across borders.

The introduction of SEPA should increase the intensity of competition among banks and corporates for customers across borders within Europe. For consumers and organisations SEPA should mean cheaper, more efficient and faster payment transfers when moving euros from one Eurozone country to another.

In Regulation (EC) 924/2009, the European Parliament mandated that charges in respect of cross-border payments (of up to EUR 50,000) to other Member States shall be the same as the charges for corresponding national payments.[9][10] However, the EU Regulation does not apply to all SEPA countries; the most significant difference is the inclusion of Switzerland in SEPA but not the EU. The rule of the same price applies, even if the transaction is sent as an international transaction instead of a SEPA transaction (common before 2008, or if any involved bank does not support SEPA transactions).

The Single Euro Payment System could be viewed as the precursor to the set up of an international, global business and trade system utilizing cashless transactions (cryptocurrency). As it is adopted in the European Union and becomes fine-tuned, it will become the standard imposed upon society as the only means to buy, sell, trade or borrow. It will eventually mutate into a total identification system that will include data necessary for travel and universal health care, etc. - Freddie Steel

Single Euro Payments Area

From Wikipedia, the free encyclopedia

| Single Euro Payments Area | ||||

|---|---|---|---|---|

|

||||

![Location of Single Euro Payments Area (dark blue)in Europe (grey) — [Legend]](https://en.wikipedia.org/wiki/File:EU28_Single-Euro-Payment-Area_-2013-.svg) |

||||

| Official languages | ||||

| Member states | ||||

1 Goals

The project's aim is to improve the efficiency of cross-border payments and turn the fragmented national markets for euro payments into a single domestic one. SEPA will enable customers to make cashless euro payments to anyone located anywhere in the area, using a single bank account and a single set of payment instruments.[2]The project includes the development of common financial instruments, standards, procedures, and infrastructure to enable economies of scale. This should, in turn, reduce the overall cost to the European economy of moving capital around the region (estimated as two to three percent of total GDP).[3]

2 Overview

There are two milestones in the establishment of SEPA:- Pan-European payment instruments for credit transfers began on 28 January 2008; direct debits and debit cards became available later

- By the end of 2010, all present national payment infrastructures and payment processors were expected to be in full competition to increase efficiency through consolidation and economies of scale

The European Commission has established the legal foundation through the PSD. The commercial and technical frameworks for payment instruments were developed by the European Payments Council (EPC), made up of European banks. The EPC is committed to delivering three pan-European payment instruments:

- Credit transfers: SCT – SEPA Credit Transfer

- Direct debits: SDD – SEPA Direct Debit. Banks began offering this service on 2 November 2009.[5]

- Cards: SEPA Cards Framework

Businesses, merchants, consumers and governments are also interested in the development of SEPA. The European Associations of Corporate Treasurers (EACT), TWIST, the European Central Bank, the European Commission, the European Payments Council, the European Automated Clearing House Association (EACHA), payments processors and pan-European banking associations – European Banking Federation (EBF), European Association of Co-operative Banks (EACB) and the European Savings Banks Group (ESBG) – are playing an active role in defining the services which SEPA will deliver.

Since January 2008, banks have been switching customers to the new payment instruments. By 2010, the majority were expected to be on the SEPA framework. As a result, banks throughout the SEPA area (not just the Eurozone) need to invest in technology with the capacity to support SEPA payment instruments.

SEPA clearance is based on the IBAN bank-account identification and the SWIFT-BIC bank identifier. Domestic transactions are routed by IBAN; earlier national-designation schemes will be abolished by February 2014, providing uniform access to the new payment instruments. By February 2016 consumers must drop BIC sorting information for SEPA transactions, since it will be derived from the IBAN for all banks in the SEPA area.

Multinational businesses and banks have the opportunity to consolidate their payment processing on common platforms across the Eurozone. They will benefit from the efficiency of choosing among competing suppliers, offering a range of solutions and operating across borders.

The introduction of SEPA should increase the intensity of competition among banks and corporates for customers across borders within Europe. For consumers and organisations SEPA should mean cheaper, more efficient and faster payment transfers when moving euros from one Eurozone country to another.

3 Coverage

SEPA consists of 33 countries:[6]- All 28 member states of the European Union, including

- the 17 states that are in the Eurozone

- the 11 states which are not in the Eurozone (Bulgaria, Croatia, the Czech Republic, Denmark, Hungary, Latvia, Lithuania, Poland, Romania, Sweden, United Kingdom)

- The four European Free Trade Association member states (Iceland, Liechtenstein, Norway, Switzerland)

- Monaco

- Cyprus: Only areas controlled by the Republic of Cyprus are included; other areas claimed by the Republic of Cyprus are exempted from EU law.

- France: Everything except French Polynesia, New Caledonia, Wallis and Futuna and French Southern and Antarctic Lands is included.

- The Netherlands: Only the European part are included; the Caribbean islands are excluded.

- The United Kingdom: includes Gibraltar but excludes the Crown dependencies (Channel Islands and Isle of Man) and excludes all other British Overseas Territories.[7]

4 Misconceptions

There is a misconception that all credit transfers in the SEPA are free to the consumer,[citation needed] either by plan rules or national transposition of the Payments Services Directives. Banks and payment institutions still have the option of charging a credit-transfer fee of their choice if it is charged uniformly to all EEA participants, banks or payment institutions, domestic or foreign.[8] This is relevant for countries which do not use the euro; domestic transfers in euro by consumers are uncommon, and inflated fees might be charged.In Regulation (EC) 924/2009, the European Parliament mandated that charges in respect of cross-border payments (of up to EUR 50,000) to other Member States shall be the same as the charges for corresponding national payments.[9][10] However, the EU Regulation does not apply to all SEPA countries; the most significant difference is the inclusion of Switzerland in SEPA but not the EU. The rule of the same price applies, even if the transaction is sent as an international transaction instead of a SEPA transaction (common before 2008, or if any involved bank does not support SEPA transactions).

5 Key dates

| 1957 | Treaty of Rome creates the European Community |

|---|---|

| 1992 | Maastricht Treaty creates the euro |

| 1999 | Introduction of the euro as an electronic currency, including introduction of the RTGS system TARGET for large-value transfers |

| 2000 | Lisbon Strategy: Meeting creates European Financial Services Action Plan |

| 2001 | EC Regulation 2560/2001 harmonises fees for cross-border and domestic euro transactions |

| 2002 | Introduction of Euro banknotes and coins |

| 2003 | First pan-European ACH (PE-ACH) goes live; EC Regulation 2560/2001 comes into force for transactions up to €12,500 |

| 2006 | EC Regulation 2560 cap increases Euro transactions up to €50,000 |

| 2008 | SEPA pan-European payment instruments become operational (parallel to domestic instruments) on 28 January[11] |

| 2009 | Payment Services Directive (PSD) enacted in national laws by November |

| 2010 | SEPA payments become dominant form of electronic payments |

| 2011 | SEPA payments replace national payments in the Eurozone |

| 2014 | Current national credit transfer and direct debit procedures will expire on 1 February. Payment service providers in the euro area will only be able to settle payments using SEPA procedures[12] |

6 Progress report

The official progress report was published in March 2013.[13] In October 2010, the European Central Bank published its seventh progress report on SEPA.[14] While acknowledging some progress since the last report, the ECB expressed disappointment at the volume of work remaining to bring the SEPA to fruition and requested banks, regulators, and the software industry to continue working. The European Central Bank regards SEPA as an essential element to advance the usability and maturity of the euro. SEPA went live in January 2008, but as of May 2012 only 28.2 percent of credit transfers within Europe were executed in accordance with SEPA standards.[citation needed]7 See also

- European Payments Union

- The Structured Creditor Reference ISO 11649 will be in Rulebook 4.2

- ISO 20022 XML: technical solution behind SEPA

- Giro

Tracking You

http://blog.mysanantonio.com/terrihall/2013/10/toll-tags-tracking-big-daddy-government-coming-to-a-road-near-you/

Feds Alarm Over Shadow Banking

http://goldnews.bullionvault.com/shadow-banking-100720136

Shadow banking system

Shadow banking system

From Wikipedia, the free encyclopedia

The shadow banking system is a pejorative term for the collection of non-bank financial intermediaries that provide services similar to traditional commercial banks. It is sometimes said to include entities such as hedge funds, money market funds, structured investment vehicles (SIV), "credit investment funds, exchange-traded funds, credit hedge funds, private equity funds, securities broker dealers, credit insurance providers, securitization and finance companies."(Jones 2013)[1]

but the meaning and scope of shadow banking is disputed in academic

literature. According to Hervé Hannoun, Deputy General Manager of the Bank for International Settlements

(BIS), investment banks as well as commercial banks may conduct much of

their business in the shadow banking system (SBS), but most are not

generally classed as SBS institutions themselves.(Hannoun 2008)[2][3] At least one financial regulatory expert has said that regulated banking organizations are the largest shadow banks.[4]

The core activities of investment banks are subject to regulation and monitoring by central banks and other government institutions - but it has been common practice for investment banks to conduct many of their transactions in ways that don't show up on their conventional balance sheet accounting and so are not visible to regulators or unsophisticated investors.[5] For example, prior to the 2007-2012 financial crisis, investment banks financed mortgages through off-balance sheet (OBS), or Incognito Leverage, securitizations (e.g. asset-backed commercial paper programs) and hedged risk through off-balance sheet credit default swaps.[5] No major investment banks exist in the United States other than those that are part of the regulated banking system. (In 2008, Morgan Stanley and Goldman Sachs became bank holding companies, Merrill Lynch and Bear Stearns were acquired by bank holding companies, and Lehman Brothers declared bankruptcy.)

The volume of transactions in the shadow banking system grew dramatically after the year 2000. Its growth was checked by the 2008 crisis and for a short while it declined in size, both in the US and in the rest of the world.[6][7] In 2007 the Financial Stability Board estimated the size of the SBS in the U.S. to be around $25 trillion, but by 2011 estimates indicated a decrease to $24 trillion.[8] Globally, a study of the 11 largest national shadow banking systems found that they totaled to $50 trillion in 2007, fell to $47 trillion in 2008 but by late 2011 had climbed to $51 trillion, just over its estimated size before the crisis. Overall, the world wide SBS totalled to about $60 trillion as of late 2011.[6] In November 2012 Bloomberg reported on a Financial Stability Board report showing an increase of the SBS to about $67 trillion.[9] It is unclear to what extent various measures of the shadow banking system include activities of regulated banks, such as bank borrowing in the repo market and the issuance of bank-sponsored asset-backed commercial paper. Banks by far are the largest issuers of commercial paper in the United States, for example.

As of 2013, academic research has suggested that the true size of the shadow banking system may have been over $100 trillion as of 2012.[10]

Shadow banking institutions are typically intermediaries between investors and borrowers. For example, an institutional investor like a pension fund may be willing to lend money, while a corporation may be searching for funds to borrow. The shadow banking institution will channel funds from the investor(s) to the corporation, profiting either from fees or from the difference in interest rates between what it pays the investor(s) and what it receives from the borrower.

Hervé Hannoun, Deputy General Manager of the Bank for International Settlements(BIS) described the structure of this shadow banking system to at the annual South East Asian Central Banks (SEACEN) conference.(Hannoun 2008)[2]

This sector was worth an estimated $60 trillion in 2010, compared to prior FSB estimates of $27 trillion in 2002.[12][8] While the sector's assets declined during the global financial crisis, they have since returned to their pre-crisis peak[13] except in the United States where they have declined substantially.

A 2013 paper by Fiaschi et. al. used a statistical analysis based the deviation from the Zipf distribution of the sizes of the world's largest financial entities to infer that that the size of the shadow banking system may have been over $100 trillion in 2012.[10][14]

There are concerns that more business may move into the shadow banking system as regulators seek to bolster the financial system by making bank rules stricter.[13]

Shadow banks can also cause a buildup of systemic risk indirectly because they are interrelated with the traditional banking system via credit intermediation chains, meaning that problems in this unregulated system can easily spread to the traditional banking system. As shadow banks use a lot of short-term deposit-like funding but do not have deposit insurance like mainstream banks, a loss of confidence can lead to "runs" on these unregulated institutions.[20] Shadow banks' collateralised funding is also considered a risk because it can lead to high levels of financial leverage. By transforming the maturity of credit—such as from long-term to short term—shadow banks fueled real estate bubbles in the mid-2000s that helped cause the global financial crisis when they burst.

Leverage is considered to be a key risk feature of shadow banks, as well as traditional banks. Leverage is the means by which shadow banks and traditional banks multiply and spread risk. Money market funds are completely unleveraged and thus do not have this risk characteristic.

When Mark Carney was appointed chairman of the FSB in November, he said the global watchdog might introduce direct regulation of the shadow banking system to tackle the risks moving into this unregulated sector from the heavily supervised mainstream banking sector. According to Carney, regulating the shadow banking industry would be a top priority for the FSB, which was likely to implement hard rules for activities like securitisation and money market funds, and use registration requirements to ensure more transparency in others.

The recommendations for G20 leaders on regulating shadow banks were due to be finalised by the end of 2012. The United States and the European Union are already considering rules to increase regulation of areas like securitisation and money market funds, although the need for money market fund reforms has been questioned in the United States in light of reforms adopted by the Securities and Exchange Commission in 2010. The International Monetary Fund suggested that the two policy priorities should be to reduce spillovers from the shadow banking system to the main banking system and to reduce procyclicality and systemic risk within the shadow banking system itself.[18]

The G20 leaders meeting in Russia in September 2013, will endorse the new Financial Stability Board (FSB) global regulations for the shadow banking systems which will come into effect by 2015.(Jones 2013)[1]

In a June 2008 speech, Timothy Geithner, then President and CEO of the Federal Reserve Bank of New York, described the growing importance of what he called the "non-bank financial system": "In early 2007, asset-backed commercial paper conduits, in structured investment vehicles, in auction-rate preferred securities, tender option bonds and variable rate demand notes, had a combined asset size of roughly $2.2 trillion. Assets financed overnight in triparty repo grew to $2.5 trillion. Assets held in hedge funds grew to roughly $1.8 trillion. The combined balance sheets of the then five major investment banks totaled $4 trillion. In comparison, the total assets of the top five bank holding companies in the United States at that point were just over $6 trillion, and total assets of the entire banking system were about $10 trillion."[22]

CONTRIBUTION TO THE 2007–2012 FINANCIAL CRISIS

Economist Paul Krugman described the run on the shadow banking system as the "core of what happened" to cause the crisis. "As the shadow banking system expanded to rival or even surpass conventional banking in importance, politicians and government officials should have realized that they were re-creating the kind of financial vulnerability that made the Great Depression possible—and they should have responded by extending regulations and the financial safety net to cover these new institutions. Influential figures should have proclaimed a simple rule: anything that does what a bank does, anything that has to be rescued in crises the way banks are, should be regulated like a bank." He referred to this lack of controls as "malign neglect."[42]

One former banking regulator has said that regulated banking organizations are the largest shadow banks and that shadow banking activities within the regulated banking system were responsible for the severity of the financial crisis[4][43]

The core activities of investment banks are subject to regulation and monitoring by central banks and other government institutions - but it has been common practice for investment banks to conduct many of their transactions in ways that don't show up on their conventional balance sheet accounting and so are not visible to regulators or unsophisticated investors.[5] For example, prior to the 2007-2012 financial crisis, investment banks financed mortgages through off-balance sheet (OBS), or Incognito Leverage, securitizations (e.g. asset-backed commercial paper programs) and hedged risk through off-balance sheet credit default swaps.[5] No major investment banks exist in the United States other than those that are part of the regulated banking system. (In 2008, Morgan Stanley and Goldman Sachs became bank holding companies, Merrill Lynch and Bear Stearns were acquired by bank holding companies, and Lehman Brothers declared bankruptcy.)

The volume of transactions in the shadow banking system grew dramatically after the year 2000. Its growth was checked by the 2008 crisis and for a short while it declined in size, both in the US and in the rest of the world.[6][7] In 2007 the Financial Stability Board estimated the size of the SBS in the U.S. to be around $25 trillion, but by 2011 estimates indicated a decrease to $24 trillion.[8] Globally, a study of the 11 largest national shadow banking systems found that they totaled to $50 trillion in 2007, fell to $47 trillion in 2008 but by late 2011 had climbed to $51 trillion, just over its estimated size before the crisis. Overall, the world wide SBS totalled to about $60 trillion as of late 2011.[6] In November 2012 Bloomberg reported on a Financial Stability Board report showing an increase of the SBS to about $67 trillion.[9] It is unclear to what extent various measures of the shadow banking system include activities of regulated banks, such as bank borrowing in the repo market and the issuance of bank-sponsored asset-backed commercial paper. Banks by far are the largest issuers of commercial paper in the United States, for example.

As of 2013, academic research has suggested that the true size of the shadow banking system may have been over $100 trillion as of 2012.[10]

1 ENTITIES THAT MAKE UP THE SYSTEM

Shadow institutions typically do not have banking licenses and don't take deposits like a depository bank and therefore are not subject to the same regulations. Complex legal entities comprising the system include hedge funds, structured investment vehicles (SIV), special purpose entity conduits (SPE), money market funds, repurchase agreement (repo) markets and other non-bank financial institutions.[11] Many shadow banking entities are sponsored by banks or are affiliated with banks through their subsidiaries or parent bank holding companies. The inclusion of money market funds in the definition of shadow banking has been questioned in view of their relatively simple structure and the highly regulated and unleveraged nature of these entities, which are considered safer, more liquid, and more transparent than banks.Shadow banking institutions are typically intermediaries between investors and borrowers. For example, an institutional investor like a pension fund may be willing to lend money, while a corporation may be searching for funds to borrow. The shadow banking institution will channel funds from the investor(s) to the corporation, profiting either from fees or from the difference in interest rates between what it pays the investor(s) and what it receives from the borrower.

Hervé Hannoun, Deputy General Manager of the Bank for International Settlements(BIS) described the structure of this shadow banking system to at the annual South East Asian Central Banks (SEACEN) conference.(Hannoun 2008)[2]

"With the development of the originate-to-distribute model, banks and other lenders are able to extend loans to borrowers and then to package those loans into ABSs, CDOs, asset-backed commercial paper (ABCP) and structured investment vehicles (SIVs). These packaged securities are then sliced into various tranches, with the highly rated tranches going to the more risk-averse investors and the subordinate tranches going to the more adventurous investors."The shadow banking system makes up 25 to 30 percent of the total financial system, according to the Financial Stability Board (FSB), a regulatory task force for the world's group of top 20 economies (G20).

—Hannoun, 2008

This sector was worth an estimated $60 trillion in 2010, compared to prior FSB estimates of $27 trillion in 2002.[12][8] While the sector's assets declined during the global financial crisis, they have since returned to their pre-crisis peak[13] except in the United States where they have declined substantially.

A 2013 paper by Fiaschi et. al. used a statistical analysis based the deviation from the Zipf distribution of the sizes of the world's largest financial entities to infer that that the size of the shadow banking system may have been over $100 trillion in 2012.[10][14]

There are concerns that more business may move into the shadow banking system as regulators seek to bolster the financial system by making bank rules stricter.[13]

1.1 SHADOW BANKS ROLE AND THEIR MODUS OPERANDI

Like regular banks, shadow banks provide credit and generally increase the liquidity of the financial sector. Yet unlike their more regulated competitors, they lack access to central bank funding or safety nets such as deposit insurance and debt guarantees.(2009 Hall)[13][15] In contrast to traditional banks, shadow banks do not take deposits. Instead, they rely on short-term funding provided either by asset-backed commercial paper or by the repo market, in which borrowers in substance offer collateral as security against a cash loan, through the mechanism of selling the security to a lender and agreeing to repurchase it at an agreed time in the future for an agreed price.[13] Money market funds do not rely on short-term funding; rather, they are investment pools that provide short-term funding by investing in short-term debt instruments issued by banks, corporations, state and local governments, and other borrowers. The shadow banking sector operates across the American, European, and Chinese financial sectors,[16](Boesler 2012)[17] and in perceived tax havens worldwide.[13] Shadow banks can be involved in the provision of long-term loans like mortgages, facilitating credit across the financial system by matching investors and borrowers individually or by becoming part of a chain involving numerous entities, some of which may be mainstream banks.[13] Due in part to their specialized structure, shadow banks can sometimes provide credit more cost-efficiently than traditional banks.[13] A headline study by the International Monetary Fund defines the two key functions of the shadow banking system as securitization – to create safe assets, and collateral intermediation – to help reduce counterparty risks and facilitate secured transactions.[18] In the US, prior to the 2008 financial crisis, the shadow banking system had overtaken the regular banking system in supplying loans to various types of borrower; including businesses, home and car buyers, students and credit users.[19] As they are often less risk averse than regular banks, entities from the shadow banking system will sometimes provide loans to borrowers who might otherwise be refused credit.[13] Money market funds are considered more risk averse than regular banks and thus lack this risk characteristic.1.2 RISKS ASSOCIATED WITH SHADOW BANKING

As shadow banks do not take deposits, they are subject to less regulation than traditional banks. They can therefore increase the rewards they get from investments by leveraging up much more than their mainstream counterparts and this can lead to risks mounting in the financial system. Unregulated shadow institutions can be used to circumvent the strictly regulated mainstream banking system and therefore avoid rules designed to prevent financial crises. Money market funds are highly regulated under the Investment Company Act of 1940, which imposes stricter regulation than banking regulation.Shadow banks can also cause a buildup of systemic risk indirectly because they are interrelated with the traditional banking system via credit intermediation chains, meaning that problems in this unregulated system can easily spread to the traditional banking system. As shadow banks use a lot of short-term deposit-like funding but do not have deposit insurance like mainstream banks, a loss of confidence can lead to "runs" on these unregulated institutions.[20] Shadow banks' collateralised funding is also considered a risk because it can lead to high levels of financial leverage. By transforming the maturity of credit—such as from long-term to short term—shadow banks fueled real estate bubbles in the mid-2000s that helped cause the global financial crisis when they burst.

Leverage is considered to be a key risk feature of shadow banks, as well as traditional banks. Leverage is the means by which shadow banks and traditional banks multiply and spread risk. Money market funds are completely unleveraged and thus do not have this risk characteristic.

1.3 Recent attempts to regulate the shadow banking system

In the United States the Dodd-Frank Act, passed in 2010, made provisions which go some way towards regulating the shadow banking system by stipulating that the Federal Reserve System would have the power to regulate all institutions of systemic importance, for example. Other provisions include registration requirements for advisers of hedge funds which have assets totalling more than $150 million and a requirement for the bulk of over-the-counter derivatives trades to go through exchanges and clearing houses.When Mark Carney was appointed chairman of the FSB in November, he said the global watchdog might introduce direct regulation of the shadow banking system to tackle the risks moving into this unregulated sector from the heavily supervised mainstream banking sector. According to Carney, regulating the shadow banking industry would be a top priority for the FSB, which was likely to implement hard rules for activities like securitisation and money market funds, and use registration requirements to ensure more transparency in others.

The recommendations for G20 leaders on regulating shadow banks were due to be finalised by the end of 2012. The United States and the European Union are already considering rules to increase regulation of areas like securitisation and money market funds, although the need for money market fund reforms has been questioned in the United States in light of reforms adopted by the Securities and Exchange Commission in 2010. The International Monetary Fund suggested that the two policy priorities should be to reduce spillovers from the shadow banking system to the main banking system and to reduce procyclicality and systemic risk within the shadow banking system itself.[18]

The G20 leaders meeting in Russia in September 2013, will endorse the new Financial Stability Board (FSB) global regulations for the shadow banking systems which will come into effect by 2015.(Jones 2013)[1]

2 Importance

Many "shadow bank"-like institutions and vehicles have emerged in American and European markets, between the years 2000 and 2008, and have come to play an important role in providing credit across the global financial system.[5][21]In a June 2008 speech, Timothy Geithner, then President and CEO of the Federal Reserve Bank of New York, described the growing importance of what he called the "non-bank financial system": "In early 2007, asset-backed commercial paper conduits, in structured investment vehicles, in auction-rate preferred securities, tender option bonds and variable rate demand notes, had a combined asset size of roughly $2.2 trillion. Assets financed overnight in triparty repo grew to $2.5 trillion. Assets held in hedge funds grew to roughly $1.8 trillion. The combined balance sheets of the then five major investment banks totaled $4 trillion. In comparison, the total assets of the top five bank holding companies in the United States at that point were just over $6 trillion, and total assets of the entire banking system were about $10 trillion."[22]

CONTRIBUTION TO THE 2007–2012 FINANCIAL CRISIS

Main article: Great Recession

The shadow banking system has been implicated as significantly contributing to the global financial crisis of 2007–2012.[5][39][40][41]

In a June 2008 speech, U.S. Treasury Secretary Timothy Geithner, then

President and CEO of the New York Federal Reserve Bank, placed

significant blame for the freezing of credit markets on a "run" on the

entities in the shadow banking system by their counterparties. The rapid

increase of the dependency of bank and non-bank financial institutions

on the use of these off-balance sheet entities to fund investment

strategies had made them critical to the credit markets underpinning the

financial system as a whole, despite their existence in the shadows,

outside of the regulatory controls governing commercial banking

activity. Furthermore, these entities were vulnerable because they

borrowed short-term in liquid markets to purchase long-term, illiquid

and risky assets. This meant that disruptions in credit markets would

make them subject to rapid deleveraging, selling their long-term assets

at depressed prices.[22]Economist Paul Krugman described the run on the shadow banking system as the "core of what happened" to cause the crisis. "As the shadow banking system expanded to rival or even surpass conventional banking in importance, politicians and government officials should have realized that they were re-creating the kind of financial vulnerability that made the Great Depression possible—and they should have responded by extending regulations and the financial safety net to cover these new institutions. Influential figures should have proclaimed a simple rule: anything that does what a bank does, anything that has to be rescued in crises the way banks are, should be regulated like a bank." He referred to this lack of controls as "malign neglect."[42]

One former banking regulator has said that regulated banking organizations are the largest shadow banks and that shadow banking activities within the regulated banking system were responsible for the severity of the financial crisis[4][43]

Are We All Internationalists?

http://newint.org/blog/internationalists/2013/10/23/we-are-all-internationalists-now/

Bilderberg Chair Visits Romania

http://www.romania-insider.com/bilderberg-group-chairman-viscount-davignon-visits-romania-meets-local-officials-business-people/108131/

India-Russia Economic Strategy

http://zeenews.india.com/business/news/international/india-russia-agree-on-brics-economic-cooperation-strategy_87352.html

Single Payment System To Be The Standard

http://m.us.wsj.com/articles/SB10001424052702304799404579155242624329108?mg=reno64-wsj

Tuesday, October 22, 2013

New Reserve Currency Pool Emerging

http://www.ibtimes.com/brics-may-decide-100b-reserve-fund-early-2014-1423462

Saturday, October 19, 2013

Canada - Europe Trade Agreement

http://mobile.nytimes.com/2013/10/19/business/international/canada-and-europe-reach-tentative-trade-agreement.html

Beware Cashless Canadians

http://business.financialpost.com/2013/10/05/the-end-of-cash-will-it-make-spending-zombies-of-us-all/

Secure Government ID Solutions

http://www.cso.com.au/mediareleases/17576/hid-global-joins-secure-identity-alliance-to/

Wednesday, October 16, 2013

US Prepares To Bury The Dollar

http://english.pravda.ru/business/finance/15-10-2013/125913-usa_budget_crisis_dollar-0/

5 Ways Government Default Would Affect You

http://m.csmonitor.com/Business/2013/1016/US-debt-default-five-ways-it-would-affect-you/Retirees-delayed-Social-Security-payments

Wednesday, October 9, 2013

Tuesday, October 8, 2013

The Future of Cryptocurrency

http://www.investopedia.com/articles/forex/091013/future-cryptocurrency.asp

Friday, October 4, 2013

Thursday, October 3, 2013

Bank CEOs Warn President

"Bank CEOs warn of consequences from U.S. shutdown, default" http://feedly.com/k/19i6bpQ

Wednesday, October 2, 2013

Nations Merge

http://www.nationalpost.com/m/wp/full-comment/blog.html?b=fullcomment.nationalpost.com/2013/09/30/diane-francis-the-merger-of-the-century

Canada's Digital Currency Being Tested

http://www.financialpost.com/m/wp/news/fp-street/blog.html?b=business.financialpost.com/2013/09/19/canadian-mint-pushes-ahead-in-murky-world-of-crypto-currency-with-mintchip-project

Monday, September 23, 2013

What Angela Merkel's Win Means To Israel

http://www.jpost.com/International/What-does-Angela-Merkels-election-win-mean-for-Israel-326812

Friday, September 20, 2013

Thursday, September 19, 2013

Banking Union Is Nail In Coffin Of Eurozone

http://rt.com/business/eurozone-banking-union-coffin-061/

Sunday, September 15, 2013

Saturday, September 14, 2013

Worst Economies In The World

http://www.usatoday.com/story/money/business/2013/09/13/worst-economies-in-the-world/2811921/

Al-Qaeda's Economic Boycott Of America

http://www.usatoday.com/story/news/world/2013/09/13/al-qaeda-economic-boycott-audio-message/2811663/

Friday, September 13, 2013

Sanctions Against Iran 'Unacceptable' Says Shanghai Cooperation Organization

http://rt.com/news/nuclear-iran-sco-summit-833/

Putin Fears We Are Out To Get Him

http://swampland.time.com/2013/09/13/why-vladimir-putin-thinks-were-out-to-get-him/?iid=tl-main-mostpop2

Thursday, September 12, 2013

Saturday, September 7, 2013

IBM Changes Retirees' Health Care Package

http://thehill.com/blogs/healthwatch/medicare/320839-ibm-to-shift-retirees-to-healthcare-exchange-due-to-rising-costs-

Friday, September 6, 2013

Thursday, September 5, 2013

'Crisis In Syria and Implications for Israel' by Rev. Jerry Clark

Commentary by Rev. Jerry Clark of Jerry Clark Ministries

https://soundcloud.com/pastor-jerry/crisis-in-syria-will-america

https://soundcloud.com/pastor-jerry/crisis-in-syria-will-america

Tuesday, September 3, 2013

Nigerian Christians Gunned Down

Nigerian Islamists gun down 5 Christians after they declare their faith - Washington Times

Error

shared via www.newshog.co

Russia, Washington, Syria And Peace

A Russian peace mission to Washington over Syria? - Christian Science Monitor

http://tinyurl.com/keupz85

shared via www.newshog.co

President Eins Backing For Syria Strike

Syria crisis: Obama wins backing for military strike - BBC News

http://tinyurl.com/nl52e5z

shared via www.newshog.co

Monday, September 2, 2013

Pulling Money Out Of Banks

http://www.dailyfinance.com/2013/09/02/out-of-the-frying-pan-into-the-market-americans-pulling-money/

Friday, August 30, 2013

The World According To Global Power Brokers

http://rt.com/op-edge/world-economy-power-brokers-forum-996/

Thursday, August 29, 2013

Shadow Banks To Comply With Global Rules

"'Shadow' banks face 2015 deadline to comply with first global rules" http://feedly.com/k/16UspuC

Syria Christians' Uncertain Future

"As Western Powers Debate Military Action, Syria Christians Face Uncertain Future" http://feedly.com/k/1ckPPeI

Bitcoins Counter Regulators

"Bitcoin aims to counter regulatory pressure" http://feedly.com/k/1ckPxnU

The Single Market And The Banking Union

"ECB: The single market and banking union" http://feedly.com/k/1dtGq8B

Tuesday, August 27, 2013

Globalization and Keynesianism

Globalization and Keynesianism - New York Times (blog)

http://tinyurl.com/k4o6utn

shared via www.newshog.co

Monday, August 26, 2013

Regulators Look At Shadow Banking

http://m.economictimes.com/news/international-business/regulators-turn-attention-to-shadow-banks/articleshow/22062524.cms

North American Union

http://www.thenewamerican.com/world-news/north-america/item/16345-north-american-union-from-nafta-to-the-nau

'The World' According To Global Power Brokers

http://rt.com/op-edge/world-economy-power-brokers-forum-996/

Guards Escort Children To Chicago Schools

http://abcnews.go.com/m/story?id=20066604&ref=http%3A%2F%2Fnews.google.com%2F

Saturday, August 24, 2013

Commercial Banks As Creators Of Money

http://mobile.nytimes.com/blogs/krugman/2013/08/24/commercial-banks-as-creators-of-money/?_r=0&

Wednesday, August 21, 2013

Saturday, August 10, 2013

Digital Money Laundering

http://qz.com/113921/you-cant-stop-digital-money-laundering-until-you-stop-secret-companies/

Friday, July 19, 2013

Contractor Razes Wrong House!

News from @AP: Texas contractor razes house, but the wrong one: http://apne.ws/12OXoDb

Unconventional NYC Megachurch

News from @AP: Unconventional pastor leads booming NYC megachurch: http://apne.ws/1bsziHv

Student Loans 101

News from @AP: Student Loans 101: Why Uncle Sam is your banker: http://apne.ws/13Ei7cL

Chicago Toughens Law By Vote 64-0

http://progressillinois.com/quick-hits/content/2013/07/17/chicago-city-council-approves-new-assault-weapons-ban-student-safety-m

China's US Treasury Shares Holdings Hit 1.3 Trillion

http://rt.com/business/china-federal-debt-record-207/

Thursday, July 18, 2013

How PayPal Almost Erases The National Debt

How PayPal Almost Erased the National Debt and Ruined the Global Economy - National Journal (blog)

http://tinyurl.com/o8pw9rj

shared via www.newshog.co

Wednesday, July 17, 2013

Digitized Health Records On The Way

http://www.foxnews.com/health/2013/07/17/digital-health-records-may-save-some-money-study-says/

Monday, July 15, 2013

China's Shadow Banking Real Threat

http://www.npr.org/blogs/parallels/2013/06/28/196617073/chinas-shadow-banking-and-how-it-threatens-the-economy

What If Dollar No Longer World Currency

http://m.frontiersman.com/mobile/opinions/columnists/compton_s_corner/what-if-the-dollar-is-no-longer-the-world-s/article_fcd9c966-eaac-11e2-b427-0019bb2963f4.html

Global Power Project Part Five

http://truth-out.org/news/item/17563-global-power-project-part-v-banking-on-influence-with-goldman-sachs

Draghi And The Fed Weighed

http://mobile.bloomberg.com/news/2013-07-12/draghi-impotent-as-fed-trumps-ecb-on-yield-curve-euro-credit.html

British Bankers Among Wealthiest

More British bankers earn 1 million euros than in rest of EU: study

Full Article: http://reut.rs/13dW0Os

More bankers in Britain earned 1 million euros ($1.3 million) in 2011 than in the rest of the European Union combined and would easily bust a planned cap on bonuses, figures from the bloc's banking regulator showed on Monday.

Subscribe to:

Posts (Atom)